Green hydrogen and green ammonia derivative value chains

As fertilisers transition from grey hydrogen and ammonia to more costly green or blue molecules, the question is: ‘who will pay the clean premium’?

The main cost driver for price premium of green and blue fertilisers is the increased cost of clean hydrogen. However, as the amount of hydrogen in the fertiliser decreases, the impact of the higher cost for clean hydrogen diminishes. The reason is that the downstream stages to produce ammonia and ammonia derivatives remain unchanged whether they are fed with grey, blue or green hydrogen.

Added value derivatives dilute the clean premium

Added-value ammonia derivatives such as urea, ammonium sulphate (AS), diammonium phosphate (DAP), ammonium nitrate (AN) and calcium ammonium nitrate (CAN) mask the green or blue hydrogen cost to reduce the ‘clean premium’ to a more affordable level.

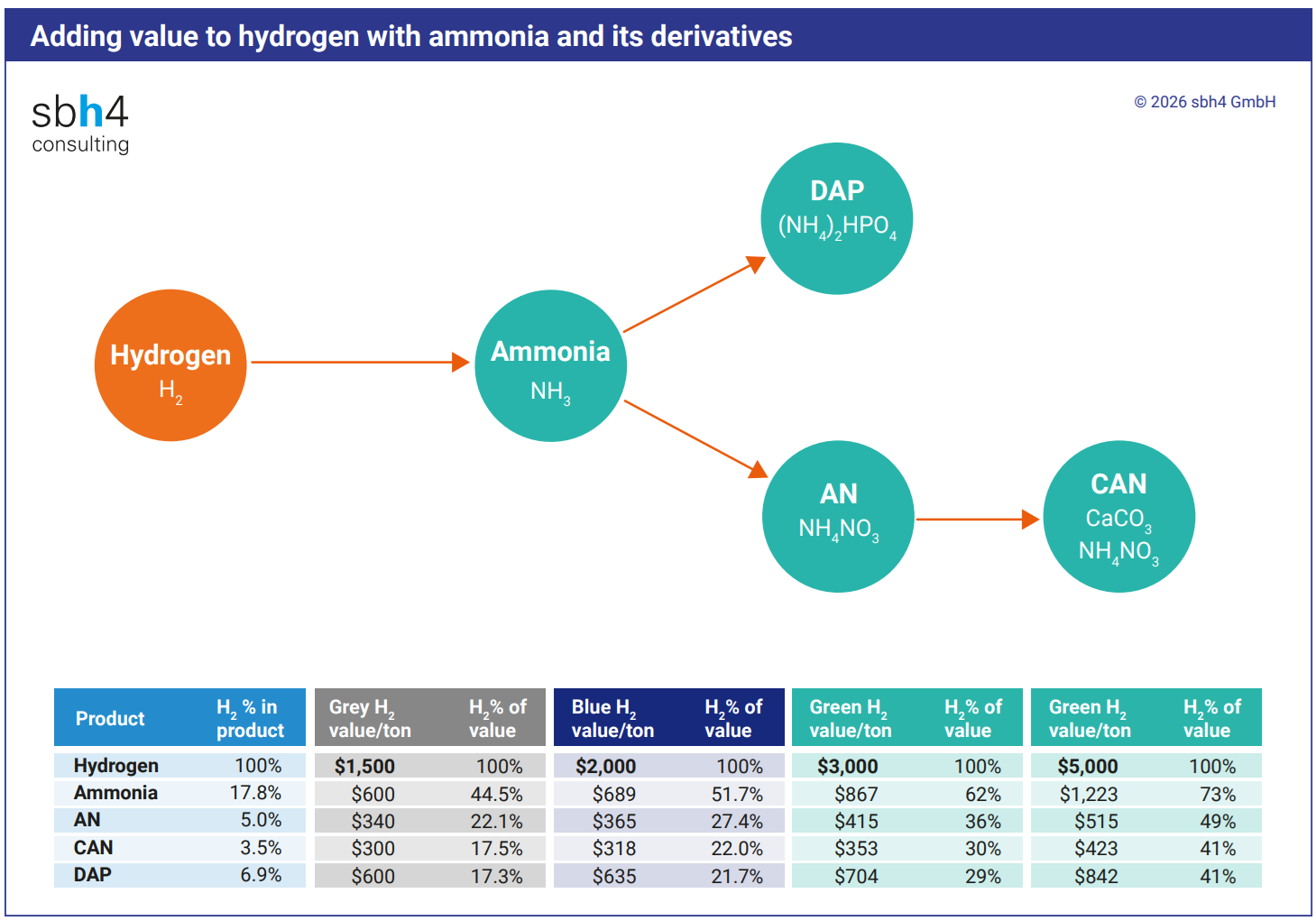

Hydrogen is 17.8% of the mass of ammonia, with nitrogen being the remainder. The hydrogen content in AN is reduced to 5%. And as the AN is converted to CAN, the hydrogen mass falls further to only 3.5%.

As the mass of hydrogen in the ammonia derivatives falls, so does its cost within the value of the product. In the case of DAP and CAN, green hydrogen[1] represents around 41% of the product value, whereas in ammonia it is 73%

Additionally, some types of solid fertiliser granules such as DAP and CAN, which are inert, can be transported more easily than liquid ammonia. In Germany, the use of AN is prohibited, opening up a high-value market for CAN.

For multiple reasons, adding value to clean ammonia through the production of ammonia derivatives can make a significant improvement in the business case for developing a clean fertiliser value chain.

High value clean ammonia derivatives projects in Paraguay

The Villeta Green Fertiliser Project is the flagship development of ATOME PLC. Villeta is a fully integrated complex, where green hydrogen production using 110MW of electrolyser capacity, ammonia synthesis, and conversion to ammonia derivatives all take place in a 30-hectare site.

Located in Puerto Sara, approximately 50 km south of Asunción, Villeta will be strategically positioned near the east bank of the Paraguay River close to the Paraguay-Paraná waterway, a regional river transport system with access to several MERCOSUR countries.

Villeta is designed to produce CAN and will require circa 170 tonnes per day of dolomite. This will be sourced from local mines, robustly integrating the facility into the Paraguayan economy.

Leveraging Villeta, ATOME is planning their second development in Paraguay: the 300 MW Yguazu project. It will diversify their product scope into other ammonia derivatives, including DAP.

ATOME’s projects are designed to reduce fertiliser imports to the MERCOSUR region and displace grey ammonia from fossil fuel reforming with green ammonia production from 100% renewable electricity.

By producing green fertiliser at or below cost parity with gas-based imports, ATOME’s projects in Paraguay serve climate goals and address the needs of the region's agricultural sector. And, by producing exportable added-value fertilisers such as CAN, the costs of green hydrogen will be absorbed to yield an internationally competitive ammonia derivative.

Bankability built around a strong business case

The techno-economic viability of green hydrogen production is almost entirely dependent on the availability and cost of electricity, which constitutes 60-70% of the green hydrogen production cost. Unlike many global green hydrogen projects that rely on intermittent wind or solar power, Villeta will utilise the 14 GW Itaipu Dam as a firm supply of green electricity.

The Villeta project utilises Casale’s Flexigreen® technology suite, which is optimized for renewable electricity-fed fertilser plants. While the Itaipu hydropower source is remarkably firm, the Flexigreen® design allows the process to turn down to 10% of nominal capacity, ensuring that the plant can adapt to grid requirements or future hybrid wind and solar renewable energy sources.

To de-risk the construction phase, in April 2025, ATOME and Casale signed a fixed-price, lump-sum EPC contract valued at $465 million. The contract guarantees that production will commence within 38 months of construction start. The use of proven technologies and the experience that Casale has in the CAN value chain maximises the bankability for lenders.

A significant commercial milestone for the project was the signing of a 10-year offtake agreement with Yara International. The agreement, finalised in September 2025, commits to purchase of the entire 260,000 tonne-per-year CAN production from Villeta. This "take-or-pay" structure serves as a fundamental pillar of the project’s bankability.

Itaipu dam control room - image courtesy of ©sbh4 GmbH

CBAM neutralises the costs of decarbonisation

When ammonia is made from steam methane reforming of natural gas, CO2 leaving the reformer must be removed prior to the catalytic Haber Bosch ammonia synthesis reaction.

The active ammonia synthesis catalyst is iron. All molecules containing oxygen, such as water, carbon monoxide and CO2 must be removed from the syngas before it is fed to the ammonia synthesis loop. Otherwise, the catalyst is oxidised and becomes ineffective. Therefore, every natural gas-fed ammonia facility integrates a CO2 capture plant.

In some facilities, about 60% of the captured CO2 is combined with ammonia to make urea. However, the residual 40% of the CO2 from the SMR (and all of the CO2 from ammonia plants that do not utilise CO2 for urea production) can be permanently sequestered.

This reduces the CO2 intensity of their downstream nitrogen fertiliser production with only a marginal incremental cost for CO2 conditioning, transportation and sequestration. With the implementation of the carbon border adjustment mechanism (CBAM) in Europe, the costs of this CO2 intensity reduction can be offset to build a business case for added-value decarbonised nitrogen fertiliser production.

Value-stacking

The idea to capture CO2 and monetise from phosphate fertiliser production will be implemented from 2027 by OCP Nutricrops in partnership with OCP Green Water and INNOVX at OCP’s Jorf Lasfar industrial platform in Morocco.

The initiative is part of OCP Group’s decarbonisation roadmap, which aims to achieve carbon neutrality across scope 1, 2 and 3 emissions by 2040. It also addresses international competitiveness by reducing the CO2 intensity of DAP which is important when exporting to the EU where the Carbon Border Adjustment Mechanism will impose tariffs on carbon-intensive imports starting in 2026.

The captured CO2 will be used by OCP Green Water for pH adjustment and re-mineralisation of drinking water in support of a local reverse osmosis desalination plant. This will support Morocco’s goal to meet 100% of the nation’s water needs through unconventional resources by 2027.

As an additional use case for the captured CO2, INNOVX will develop a plant to combine CO2 and waste phosphogypsum to produce AS. The Merseburg Process is the most common pathway to achieve this: it reacts aqueous ammonia with CO2 to produce ammonium carbonate.

Phosphogypsum is reacted with ammonium carbonate to yield calcium carbonate and the target product ammonium sulphate. Calcium carbonate is a recognised permanent sink for CO2, so this pathway sequesters CO2 emissions from the DAP process and enables integrated production of AS.

Ammonium Sulphate – the original ammonia derivative

AS was the first commercially available nitrogen fertiliser but it was displaced in many markets by ammonia and urea due to their higher nitrogen content. However, it is still used extensively in Brazil, which imports about 4 million tonnes per year, mostly from China.

AS is suitable for the Brazilian soils, which contain very low sulphur levels. Sulphur is essential to grow protein-rich crops such as soya beans, which are exported to the USA and used locally for cattle farming.

Additionally, AS has a lower ammonia volatilisation rate than urea. This is important in the warm Brazilian climate and is a factor that also leads to its use in South East Asia for growing wheat and rice.

[1] Assumes green hydrogen cost of $5,000 per tonne

***

Author credit – Stephen B. Harrison, sbh4 GmbH

sbh4 is an independent advisory firm focused on decarbonisation and defossilisation through e-fuels, e-fertilizers, biofuels, SAF, CCTUS, GHG emissions reduction, and the emerging hydrogen economy. For more information, visit www.sbh4.de.